Economic outlook and forecasts Surging gas prices shift spending, slow regional growth

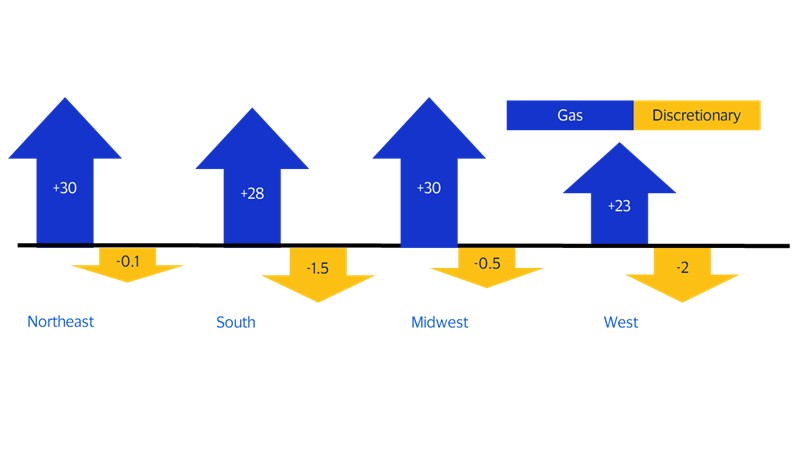

Fuel spending is displacing other spending

January to April change in SMI by category and region (NSA, Index; last actual: April 2026

Given that both the South and West tend to have higher debt-to-income (DTI) ratios than other regions,¹ we expect higher price growth and a lack of interest rate relief to disproportionately impact their economic, consumer spending and employment growth. Additionally, restrictive immigration policy is expected to have an outsized impact on employment and consumer spending growth in these regions, which saw the highest share of new immigrants from 2021-2024.²

While the Northeast and Midwest have relatively lower DTI ratios,³ higher energy and borrowing costs will likely drag on economic and consumer spending growth. Gas spending momentum has risen the most in these two regions, signaling that consumer budgets are being stretched thinner. The Midwest is likely to be hit particularly hard in the coming months, as the manufacturing sector continues to shed jobs and the region is unlikely to reap the same magnitude of tax refund benefits as the Northeast and West.

Northeast growth to hold up despite recent headwinds

Our updated forecasts continue to show the Northeast as a relative outperformer in 2026, but headwinds have emerged. Higher energy costs will likely translate into slower real spending growth this year, leading us to downwardly revise our real GDP growth forecast for 2026. Consumer confidence is also expected to remain subdued this year, consistent with a strong-spending/soft-sentiment mix tied to policy-driven income effects and higher household cost pressures.

State and Local Taxes (SALT) cap relief is still expected to boost after-tax incomes in high-income states such as New York, New Jersey, Massachusetts and Connecticut, supporting stronger consumer spending in the first half of the year. However, this tailwind is now partially offset by higher energy costs. The sharp rise in gas spending early in 2026 suggests some displacement away from discretionary categories, even in more affluent households.

State-level developments continue to provide important offsets to broader structural headwinds. In New York, Micron’s $100 billion semiconductor megafab broke ground in January 2026, marking one of the largest manufacturing investments in U.S. history and supporting a multiyear construction and supply-chain cycle tied to AI-related demand.⁴

Energy and grid investment is also rising in importance. Massachusetts’ Vineyard Wind 1 completed construction in March 2026.⁵ This development has a projected 800-MW capability, and is intended to support specialized construction, port activity, and supply-chain services.

Pennsylvania continues to stand out as a key growth node within the Northeast, benefitting from a surge in AI and infrastructure investment. Amazon announced plans to invest at least $20 billion in cloud computing and data center campuses across the state as part of a broader pipeline involving tens of billions of dollars in AI, energy and digital infrastructure projects.⁶ These developments are supporting near-term construction activity and longer-term growth in high-value services, though rising electricity demand and infrastructure constraints present emerging headwinds.

Overall, the Northeast outlook remains characterized by a front-loaded boost to spending, followed by slowing momentum later in 2026 as demographic constraints, elevated energy costs and higher interest rates weigh on growth—even as large-scale investment in semiconductors and AI infrastructure provides targeted support in key states.

Migration slowdown set to constrain growth in the South this year

Our updated forecast for the South reflects a region dealing with higher costs and a smaller workforce than in previous years. Real GDP growth has been downwardly revised, as the region transitions from a migration-led expansion to one increasingly shaped by capital investment, infrastructure demand, and cost pressures.

A key shift in 2026 is the cooling of the migration boom that defined the region’s post-pandemic strength. In Florida, population growth has slowed sharply as affordability pressures rise and both domestic and international migration moderate.⁷ Net domestic migration has fallen significantly from its earlier peak, and recent estimates show the pace of inflows has normalized. This shift is important because population inflows had been a primary driver of housing demand, labor force growth and consumption across much of the region. While large states like Florida are seeing slower net inflows, the Carolinas continue to post some of the fastest growth rates in the country. This divergence is likely to lead to more variation in housing demand, labor market tightness and consumer spending performance across the South.

At the same time, the composition of growth is shifting toward large-scale industrial and digital infrastructure investment, particularly in Texas and the Southeast. Texas is emerging as one of the largest data center markets globally, driven by AI-related demand, abundant land and access to energy resources.⁸ This expansion is already pushing power demand sharply higher, prompting accelerated investment in generation and grid capacity. This is expected to support construction, utilities and capital spending in the coming years.

Similar dynamics are playing out across the broader Southeast manufacturing corridor. In Georgia, Hyundai’s EV Metaplant is ramping up production and expanding, supporting thousands of jobs and reinforcing the region’s position as a hub for advanced manufacturing.⁹ These types of projects are helping offset slower population-driven growth by anchoring longer-term investment cycles and supplier ecosystems across multiple states.

Overall, the South in 2026 is no longer defined by rapid population inflows. Instead, growth is increasingly shaped by the interaction between large-scale capital investment and emerging constraints such as energy capacity, infrastructure needs and cost pressures. While these forces should continue to support solid regional growth, they also point to a more moderate and uneven expansion over the remainder of the year.

The heartland holds steady as manufacturing drags

The Midwest economy held its own at the end of 2025, growing 2 percent year-over-year in the fourth quarter, unchanged from the previous quarter. We expect growth to accelerate this year before mildly downshifting in 2027.

Minnesota and Indiana are carrying much of the Midwest’s growth burden, and it’s no coincidence that both states are also leading the region in healthcare employment growth and investment. Minnesota alone added more than 7,000 healthcare workers in the first quarter of 2026, while Indiana added nearly 4,000. With billions of dollars being invested in hospital expansion, biotech, and pharmaceuticals, these states are poised to continue outperforming the region in employment, consumer spending, and overall growth. But healthcare tailwinds aren’t limited to the region’s outperformers. The sector has been a bulwark for average and even underperforming states. In Ohio, for example, healthcare accounted for more than one-quarter of the state’s job growth in the first quarter of 2026. Even in states like Michigan, where payrolls have recently declined, healthcare employment is helping offset job losses elsewhere.

Nonetheless, manufacturing remains the primary factor limiting the region’s growth, particularly in states with an overreliance on the sector, such as Michigan, Wisconsin, Ohio, and even Indiana. Input costs were already high in the wake of tariffs and other trade disruptions, even before the recent surge in oil and gasoline prices. Add in elevated borrowing costs, and the operating environment has become increasingly challenging for many producers.

The region’s agricultural sector is also under increasing duress. China’s continued pullback in U.S. soybean exports is driving down prices and hurting row-crop producers in top soybean-producing states like Illinois and Iowa. Fertilizer prices have also risen sharply since the conflict with Iran began. Iran was a major exporter of nitrogen fertilizer, and the contested Strait of Hormuz is a crucial shipping route for global seaborne fertilizer trade. While strong demand and historically low herd counts are driving record prices for cattle ranchers, Midwest row-crop producers are reeling from higher input costs and weakening export prices.

Looking ahead, we expect the Midwest to lag the nation, as agricultural headwinds and manufacturing woes continue to hold back growth, even as pockets of strength in healthcare, biotech, and advanced manufacturing take root.

Growth shifts from momentum to moderation in the West

The West’s economy slowed toward the end of 2025, with regional GDP growth easing from 2.5 percent year over year in the third quarter to 2 percent in the fourth. States across the region face uneven job growth, mixed demographic trends, softer tourism, and higher energy costs. While AI-related investment should keep growth near the top of regional rankings in 2026—second only to the Northeast—these headwinds are expected to intensify. As a result, growth in the West is projected to fall behind both the Northeast and the South by 2027.

The AI boom is supporting growth in the region’s major tech hubs, but heavy capital spending is prompting firms to cut costs elsewhere, raising uncertainty about longer-term impacts. For example, two of Washington’s largest tech firms announced sizable headcount reductions this year, and tech employment there has been essentially flat since 2024. In contrast, manufacturing employment—particularly in transportation equipment and advanced manufacturing—has risen alongside improved demand and a temporary easing of trade tensions with China.

Similar uncertainty surrounds California’s tech sector, which continues to adjust after post-pandemic overhiring. Tech employment in the state remains below pre-pandemic averages. For now, healthcare and AI-related hiring are supporting job growth, but California is likely to lag in 2027 as AI investment reshapes, rather than expands, tech employment.

Tourism-dependent states were already seeing slower travel demand before the surge in fuel prices and now face an even weaker outlook. Visitor numbers for Las Vegas declined last year for the first time since the pandemic, and higher airfares and gasoline prices point to continued softness in 2026. Still, strong migration and population growth should offset some of these pressures. Nevada, for instance, is benefiting from robust nonresidential investment, particularly in data centers and logistics, while Hawaii’s reliance on tourism and ongoing population losses will keep it underperforming.

Arizona, Utah, and Idaho remain key growth engines, supported by strong migration that is boosting population, investment, and high-wage job creation. These states will underpin regional growth in 2026, but over the longer term the West is expected to underperform the U.S. economy due to tech sector restructuring, higher energy and financing costs, and persistent affordability constraints in coastal markets.

Footnotes

- Visa Business and Economic Insights and The U.S. Department of Commerce

- Visa Business and Economic Insights and The Federal Reserve Board

- Visa Business and Economic Insights and The Federal Reserve Board

- Visa Business and Economic Insights and Office of the Governor of New York, From Promise to Progress: Governor Hochul Celebrates Groundbreaking of Micron’s Semiconductor Manufacturing Facility in Central New York, January 16, 2026

- Visa Business and Economic Insights and WBUR, Vineyard Wind, country's first large-scale offshore wind project, finishes construction, March 14, 2026

- Visa Business and Economic Insights and The Associated Press, Amazon to spend $20B on data centers in Pennsylvania, including one next to a nuclear power plant, June 9, 2025

- Visa Business and Economic Insights and Axios, Florida migration boom fades as rising costs push residents out, April 30, 2026

- Visa Business and Economic Insights and Texas Tribune, Texas forecast to be top market for data centers in two years, increasing grid demand, January 20, 2026

- Visa Business and Economic Insights and CBT News, Inside Hyundai’s $7.6 billion EV power play: A first look at the MetaPlant America Revolution, May 14, 2026

Forward-Looking Statements

This report may contain forward-looking statements within the meaning of the U.S. Private Securities Litigation Reform Act of 1995. These statements are generally identified by words such as “outlook”, “forecast”, “projected”, “could”, “expects”, “will” and other similar expressions. Examples of such forward-looking statements include, but are not limited to, statements we make about Visa’s business, economic outlooks, population expansion and analyses. All statements other than statements of historical fact could be forward-looking statements, which speak only as of the date they are made, are not guarantees of future performance and are subject to certain risks, uncertainties and other factors, many of which are beyond our control and are difficult to predict. We describe risks and uncertainties that could cause actual results to differ materially from those expressed in, or implied by, any of these forward-looking statements in our filings with the SEC. Except as required by law, we do not intend to update or revise any forward-looking statements as a result of new information, future events or otherwise.

Disclaimers

The views, opinions, and/or estimates, as the case may be (“views”), expressed herein are those of the Visa Business and Economic Insights team and do not necessarily reflect those of Visa executive management or other Visa employees and affiliates. This presentation and content, including estimated economic forecasts, statistics, and indexes are intended for informational purposes only and should not be relied upon for operational, marketing, legal, technical, tax, financial or other advice and do not in any way reflect actual or forecasted Visa operational or financial performance. Visa neither makes any warranty or representation as to the completeness or accuracy of the views contained herein, nor assumes any liability or responsibility that may result from reliance on such views. These views are often based on current market conditions and are subject to change without notice.

Visa’s team of economists provide business and economic insights with up-to-date analysis on the latest trends in consumer spending and payments. Sign up today to receive their regular updates automatically via email.